How Banks Calculate Your Car Payment

Table of Contents

- How Much Will My Car Payment Be? How Banks Calculate Your Maximum

- The Four Factors That Determine Your Monthly Payment

- How Lenders Decide the Maximum They'll Approve

- Payment-to-Income (PTI) Ratio

- Debt-to-Income (DTI) Ratio

- What You Can Control to Get a Better Payment

- Short Term vs. Long Term — The Trade-Off

- Why Estimated Payments Online Are Just a Starting Point

- Let Us Run the Numbers for You

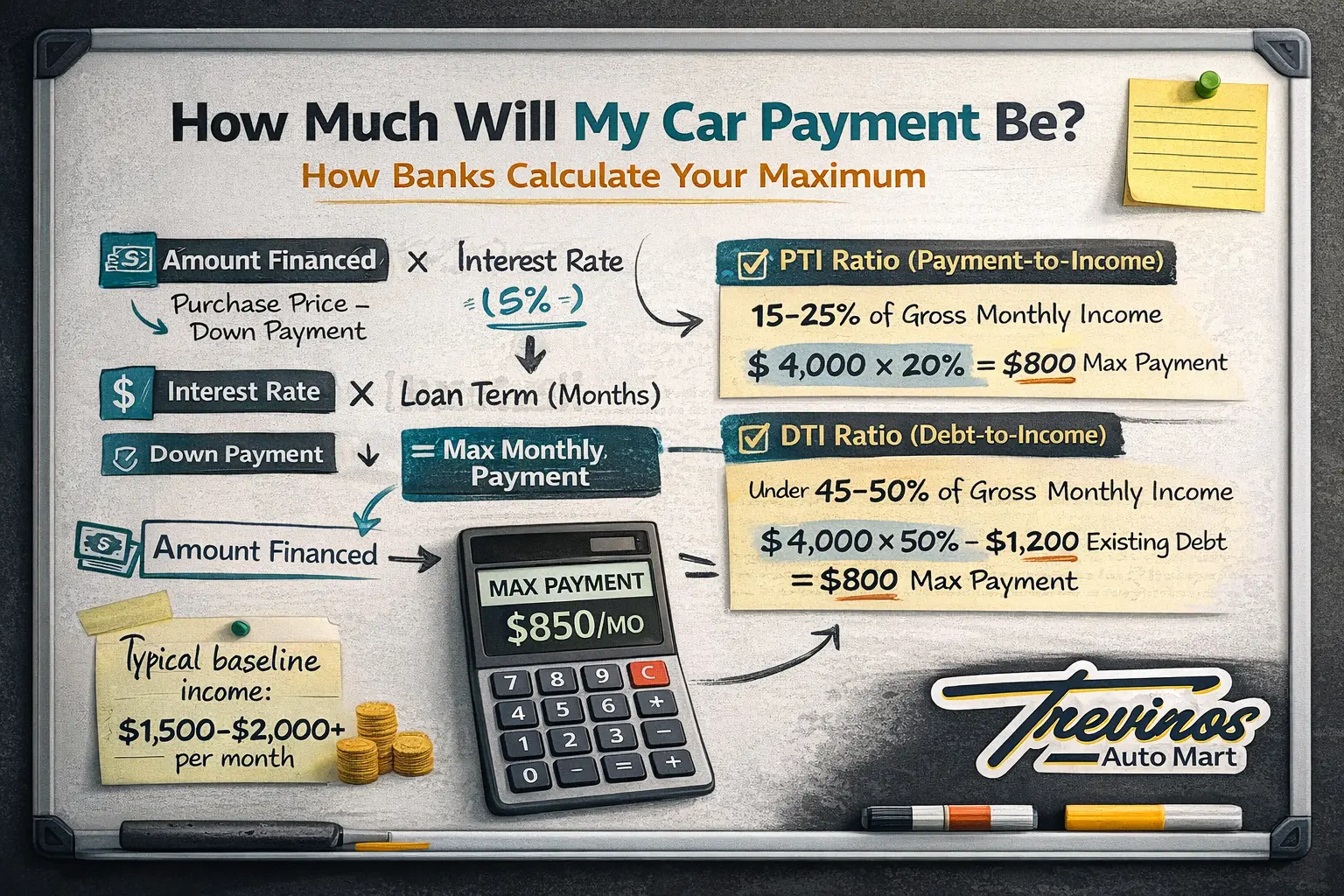

How Much Will My Car Payment Be? How Banks Calculate Your Maximum

Ever wonder how a lender decides what payment you can afford? Here's the behind-the-scenes math banks use — explained in plain English.

When you apply for a car loan, the lender doesn't just pick a random number and say "this is your payment." There's actual math behind it — and once you understand how it works, you can put yourself in a much stronger position before you ever walk into a dealership.

Here's how banks and lenders figure out your car payment.

The Four Factors That Determine Your Monthly Payment

Every car payment comes down to four variables. Change any one of them and your payment changes too:

- Amount financed. This is the vehicle cost minus your down payment and trade-in value, plus any taxes, fees, and optional products (like a protection plan). The less you finance, the lower your payment.

- Interest rate (APR). This is the cost of borrowing money, expressed as a percentage. Your rate depends primarily on your credit profile, the lender, and the vehicle. Lower rate = lower payment.

- Loan term. How long you have to pay it back, measured in months. Common terms are 48, 60, 72, and 84 months. A longer term means a lower monthly payment — but more total interest paid over time.

- Down payment / trade-in. Whatever you put down upfront comes off the amount financed, which directly reduces your payment.

The simple version: Lower amount financed + lower interest rate + reasonable loan term = a payment you can live with.

How Lenders Decide the Maximum They'll Approve

Beyond calculating the payment itself, lenders set a maximum based on your ability to repay. They typically look at two key ratios:

Payment-to-Income (PTI) Ratio

This is your proposed car payment divided by your gross monthly income. Most lenders cap this at 15–20%, though some will go as high as 25% for strong applicants.

Example: If you earn $4,000/month gross, a lender with a 20% PTI cap would approve a maximum car payment of $800/month.

Debt-to-Income (DTI) Ratio

This is all of your monthly debt payments (car payment, rent/mortgage, credit cards, student loans, etc.) divided by your gross monthly income. Most auto lenders want this under 45–50%.

Example: If you earn $4,000/month and already pay $1,000 in rent and $200 in credit card minimums, your existing DTI is 30%. A lender with a 50% DTI cap would allow up to $800/month in additional debt — but your PTI cap might limit you before you hit that number.

The lender uses whichever ratio is more restrictive to set your maximum. This is why paying off even one small debt before applying can open up a better approval.

What You Can Control to Get a Better Payment

You can't change the interest rate formula, but you can influence the inputs. Here's where you have leverage:

- Increase your down payment. More down = less financed = lower payment. This is the most direct lever you can pull. If you have a trade-in, that counts too. Check your trade-in value online.

- Choose a vehicle that fits your budget. Falling in love with a vehicle before knowing your numbers is how people end up with uncomfortable payments. Start with the payment, then find the vehicle.

- Reduce existing debt before applying. Paying off a credit card or small loan improves your DTI ratio, which can increase your approved amount or get you better terms.

- Apply with a co-borrower. Adding someone with good credit or additional income to the application can improve both your rate and your approved amount.

- Shop your application across multiple lenders. Different lenders offer different rates and terms for the same applicant. This is where working with a dealership like Trevino's pays off — we submit to multiple lenders and find you the best deal.

Short Term vs. Long Term — The Trade-Off

One of the biggest decisions in car financing is the loan length. Here's the honest trade-off:

- Shorter term (36–48 months): Higher monthly payment, but you pay less interest overall and own the vehicle outright sooner. Best if you can handle the higher payment comfortably.

- Medium term (60 months): The most popular choice. Balances an affordable payment with a reasonable total interest cost. This is where most of our customers land.

- Longer term (72–84 months): Lowest monthly payment, but you'll pay significantly more in interest over the life of the loan. You also risk being "upside down" for longer, meaning you owe more than the vehicle is worth. This can be a problem if you need to trade in or sell before the loan is paid off.

There's no single right answer — it depends on your budget, your goals, and how long you plan to keep the vehicle. Our finance team can show you multiple scenarios so you can make the best call.

Why Estimated Payments Online Are Just a Starting Point

When you browse our inventory, you'll see an estimated monthly payment on every listing. These estimates give you a useful ballpark, but your actual payment will depend on your specific credit profile, the rate you qualify for, your down payment, and the loan term you choose.

The only way to know your real numbers is to apply. You can apply online in about five minutes, and our finance team will come back with real figures based on your situation — not estimates.

Let Us Run the Numbers for You

At Trevino's Auto Mart, we don't play payment games. We'll sit down with you, explain exactly how the numbers work, and show you options that fit your budget. Multiple lenders, transparent terms, and a team that's been doing this since 1992.

Come by, give us a call, or start online. No pressure — just real numbers.

Trevino's Auto Mart

2409 S 23rd Street, McAllen, TX 78503

(956) 686-7522

Monday – Friday: 9:30 AM – 6:30 PM | Saturday: 9:30 AM – 4:00 PM

Trevino's Auto Mart proudly serves McAllen, Mission, Pharr, Edinburg, Weslaco, Harlingen, Brownsville, and all of the Rio Grande Valley.